http://www.bloomberg.com/video/the-european-debt-crisis-visualized-iPA3~AbsSGG89LOGkkd~RA.html

http://www.bloomberg.com/video/the-european-debt-crisis-visualized-iPA3~AbsSGG89LOGkkd~RA.html

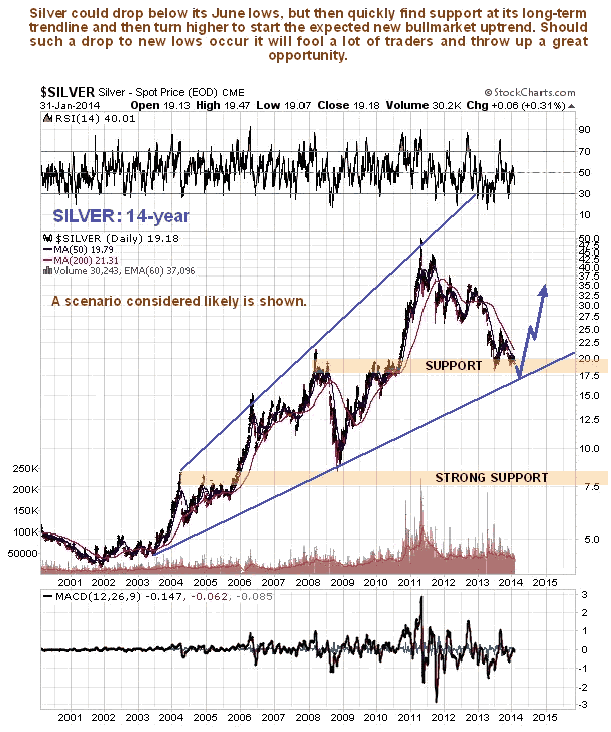

Our general view is Japan is likely to go higher as the currency weakens, however without any serious reform Japan will hit the wall and stagnate (unlikely the place to be longer term). Europe will continue to experience deflation and more social unrest as the policies of government continue to drag the economy to its knees. Emerging markets with will low debt will perform better than others. The US dollar is very oversold and is due for a rally (the world’s core economy has never seen hyperinflation in any period of history) As interest rates rise this will bring on more fear of government and their ability to pay interest on Debt. This is when you will see gold rally to new all time highs in the next 3~5 years.

I believe that gold will bottom in 2014. In a Fed tightening cycle, gold tends to go down. Financial players in this cycle have been impatient to kick gold down as hard as possible. They short gold producers first and then gold. The gold stocks are much bigger in value than gold market per se. Hence, the trading strategy of shorting gold stocks and then gold could be lucrative. As more and more people pursue the same trade, the gold is kicked down way beyond its fundamentals.

Gold demand is from emerging economies. The latter have been experiencing high inflation. The demand for gold has been strong despite the weak gold price in 2013. The current gold price is already below the production cost of some of the biggest mines in the world. I suspect that, in 2014, some mines may be shut. The reduction in supply will become a counterforce against the Fed’s tightening.

I want to repeat my long term bullish call on gold. Its price is likely to top US$ 3,000 in five years. The currency market instability and the likely global stagflation will strengthen gold demand for wealth preservation in emerging economies. As supply is unable to grow, the price has to rise to balance the market.

Overall there will be a move from Public to Private assets and this may very surprise everyone with the short term gains we will see in the USA markets, there will be corrections and one should buy when the markets have a downdraft, perhaps this first quarter.

There is still a lot of complacency worldwide. For example, car sales have been outstanding and our guess has been that a surge of better economic reports would be part of the final surge in the stock markets.

In early July, things started to deteriorate as regions from Turkey to Brazil to China and Indonesia were “getting hit by a brutal combination of events, as economies slow, investors pull out cash, commodity prices tumble and protesters take to the streets”. That’s how the Wall Street Journal wrote it up on July 2nd.

The news reminded of early July 1997 when the “Asian Crisis” roiled the Thai baht. It denied establishment boasts that the problem could be “isolated”. After traveling around Asia, eventually it fetched up in New York in that fateful September when the corporate bond market suffered its worst month in a decade.

This time around, the “Asian” problem started in early-July and on August 29th Bloomberg reported “Stocks in Southeast Asia are tumbling at the fastest pace in 12 years relative to global equities”.

A chart of the Indonesian Stock Market

This has been accompanied by continued weakness in Emerging Market bonds (EMB), which makes sense. US Munis (MUB) also continue to decline and the Spanish Ten-Year yield is turning up. At the close it was up to 4.62%. Rising above 4.48% is a breakout. Lower-grade corporates (HYG and JNK) became oversold a couple of weeks ago and have rallied to resistance.

In Japan, the government has indebted itself to the tune of 230% of GDP… a total exceeding ONE QUADRILLION yen.

That’s a “1 with 15 zer000000000000000‘s after it. 1,000,000,000,000,000

And according to the Japanese government’s own figures, they spent a mind-boggling 24.3% of their entire national tax revenue just to pay interest on the debt last year!

Remember this adds a minimum 25 trillion more debt each year just on interest! Not to mention the other (again at minimum) 30 trillion in deficit spending to keep the wheels on Japan. The net minimum increase in annual debt is about 55 Trillion! At least!

Slowly, somewhere between this untenable fiscal position and the radiation leak at Fukushima, a few Japanese people realized that their confidence in the system was misguided.

We are helping an increasing number Japanese residents send some funds offshore.

Why? If the government defaults on its debts or ignites a currency crisis (both likely scenarios given the raw numbers), then those folks will at least preserve a portion of their savings intact. But if nothing happens and Japan limps along, they won’t be worse off for having some cash in a strong, stable, well-capitalized offshore banking jurisdiction. Where their funds are allocated and separated from bank assets, with no liens or encumbrances.

For Japan, the smart people who see the writing on the wall just want to be prepared with a sensible solution. They’re taking action before anything financially disastrous happens.

So what can you do?

Don’t be complacent, be prepared.

Frank Holmes of US Global Investors is another who has forgotten more about the gold market

than many will ever know.

Here is his take on how far gold is off course:

Gold has been in extremely oversold territory lately despite drivers for the metal remaining in place.

Here’s a different way to look at how far gold has been off course. The chart below tracks the correlation of the price of an ounce of gold to global liquidity, with global liquidity defined as the sum of the U.S. monetary base and the foreign holdings of U.S. Treasuries. Since June 2000, as the U.S.’s monetary base and foreign holdings increased, so did the price of gold.

The correlation suggests the current level of liquidity supports a gold price of $1,780 per ounce, well above the current spot price around $1,300.

Source: US Global Investors